Assumable Mortgage Approval Timelines are Dropping Fast

In today’s rapidly evolving real estate market, assumable mortgages have emerged as a game-changer for homebuyers seeking to save money and secure favorable financing terms. As interest rates continue to rise, the ability to assume a seller’s existing mortgage at a lower rate has become increasingly attractive.

Historically, the process of obtaining approval for an assumable mortgage has been lengthy and complex, often spanning several months. However, recent changes in the industry have led to a significant reduction in assumable mortgage approval timelines, making this option more accessible and appealing than ever before.

Understanding Assumable Mortgages

Before diving into the recent changes in approval timelines, let’s first establish a clear understanding of what an assumable mortgage is and how it differs from traditional home loans.

What is an Assumable Mortgage?

An assumable mortgage is a type of home loan that allows a buyer to take over the seller’s existing mortgage, including the current interest rate, remaining loan balance, and loan term. Instead of applying for a new mortgage, the buyer assumes responsibility for the seller’s existing loan, potentially saving thousands of dollars in interest payments over the life of the loan.

How Do Assumable Mortgages Differ from Traditional Home Loans?

- Interest Rates: Assumable mortgages allow buyers to take advantage of the seller’s existing interest rate, which may be lower than current market rates.

- Loan Terms: Buyers assume the remaining loan term of the seller’s mortgage, which could be advantageous if the seller is several years into a 30-year mortgage.

Qualification Process: While buyers still need to qualify for an assumable mortgage, the process may be more streamlined compared to applying for a new loan.

Types of Assumable Mortgages

There are three primary types of assumable mortgages:

- VA Loans: Backed by the U.S. Department of Veterans Affairs, these loans offer favorable terms and are available to eligible veterans and their spouses.

- FHA Loans: Insured by the Federal Housing Administration, these loans are assumable and offer more lenient qualification requirements compared to conventional mortgages.

USDA Loans: Designed to promote homeownership in rural areas, USDA loans are assumable and offer competitive interest rates and terms.

The Assumption Process: Past Challenges and Recent Changes

Traditionally, the process of assuming a mortgage has been a lengthy and complicated one, often deterring potential buyers from pursuing this financing option. However, recent changes in the real estate industry have streamlined the assumption process, making it faster and more efficient than ever before.

Past Challenges in the Assumption Process

- Lack of Standardization

- Limited Lender Experience

- Lengthy Approval Times

Recent Changes and Improvements

- Standardized Procedures: Lenders and servicers have adopted standardized procedures for processing assumable mortgages, reducing confusion and increasing efficiency.

- Increased Lender Education: Lenders have invested in training and education programs to ensure their staff is well-versed in handling assumable mortgages, resulting in faster processing times.

- Improved Communication: Enhanced communication channels between lenders, servicers, and government agencies have led to quicker resolution of issues and faster approval times.

VA Loans: Leading the Way in Assumable Mortgage Approval Timelines

Among the various types of assumable mortgages, VA loans have seen some of the most significant improvements in approval timelines. Thanks to recent guidance from the Department of Veterans Affairs, the process of assuming a VA loan is now faster and more straightforward than ever before.

VA Circular 26-23-27: A Game-Changer

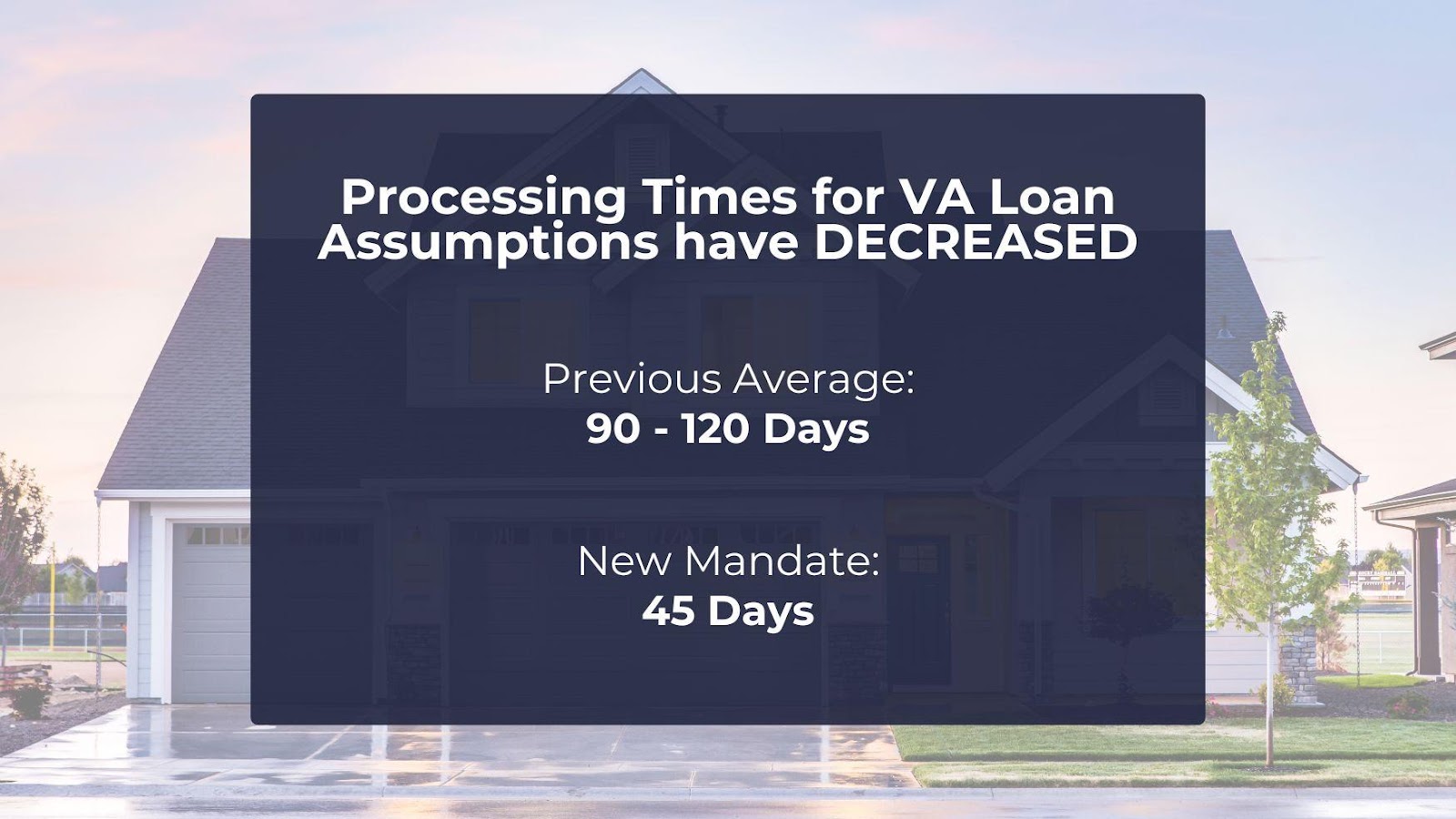

In December 2023, the VA issued Circular 26-23-27, which provided clear guidance to lenders and servicers on processing VA loan assumptions. The circular addressed several key points:

Mandated 45-Day Timeline

Lenders and servicers are now required to process VA loan assumptions within 45 days of receiving a complete application package.

Consequences for Non-Compliance

Failure to adhere to the mandated timeline can result in severe consequences for lenders, including the loss of VA guaranty on the loan.

Emphasis on Veteran Rights

The circular emphasizes the rights of veterans and buyers to assume VA loans, ensuring that the assumption process is accessible and fair.

Impact of VA Circular 26-23-27 on Approval Timelines

The effects of VA Circular 26-23-27 have been significant, with notable improvements in VA loan assumption approval timelines:

- Dramatic Reduction in Processing Times

- Increased Lender Prioritization

- Competitive Landscape

Benefits of Faster Assumable Mortgage Approval Timelines

The faster approval timelines for assumable mortgages offer significant benefits for both buyers and sellers in today’s real estate market.

Buyer Benefits

- Lower Interest Rates: By assuming a seller’s existing mortgage, buyers can secure a lower interest rate than what’s currently available in the market, potentially saving thousands of dollars over the life of the loan.

- Significant Monthly Savings: Lower interest rates translate to lower monthly mortgage payments, making homeownership more affordable and allowing buyers to allocate funds towards other financial goals.

- Reduced Closing Costs: Assuming a mortgage often involves lower closing costs and fees compared to obtaining a new loan, further increasing the savings for buyers.

Seller Benefits

- Increased Marketability: Properties with assumable mortgages become more attractive to potential buyers, especially in a rising interest rate environment, leading to faster sales and a larger buyer pool.

- Faster Sales Process: Shorter approval timelines for assumable mortgages can significantly reduce the overall sales process, allowing sellers to close deals more quickly and move on to their next chapter.

- Competitive Advantage: Offering an assumable mortgage can give sellers a competitive edge in the market, particularly when inventory is limited and buyers are seeking ways to save on financing costs.

Tips for a Smooth Assumption Process

While the assumption process has become faster and more efficient, there are still steps that buyers and sellers can take to ensure a smooth and successful transaction.

Tips for Buyers

- Work with an Experienced Lender: Partner with a lender who has a proven track record in handling assumable mortgages and is well-versed in the latest industry guidelines and requirements. AssumeList can help connect you with experienced lenders specializing in assumable mortgages.

- Gather Financial Documentation: Prepare and organize all necessary financial documents, such as income statements, tax returns, and bank statements, to streamline the qualification process.

- Be Responsive and Proactive: Promptly respond to lender requests for additional information or clarification, and proactively communicate any changes in your financial situation or employment status.

Tips for Sellers

- Confirm Mortgage Assumability: Before listing your property, confirm with your lender that your mortgage is indeed assumable and gather all relevant loan information, such as interest rate, remaining balance, and loan term.

- Work with a Knowledgeable Real Estate Agent: Partner with a real estate agent who has experience in selling properties with assumable mortgages and can effectively market your home to potential buyers. AssumeList can connect you with a qualified agent who specialize in assumable mortgage properties.

Assist the Buyer: Be prepared to assist the buyer in the assumption process, providing necessary documentation and communicating with your lender to ensure a smooth transfer of the loan.

The Future of Assumable Mortgages

As the real estate industry continues to evolve and adapt to the changing needs of homebuyers, assumable mortgages are poised to play an increasingly important role in the future of home financing.

Potential for Increased Adoption

With the demonstrated benefits of faster approval timelines and the potential for significant savings, more buyers and sellers may begin to explore assumable mortgages as a viable financing option. As awareness grows and success stories circulate, the demand for assumable mortgages is on the rise, leading to increased adoption across the industry. As more people pursue them, efficiencies in the approval process are gained.

Lender Adaptation and Innovation

As the demand for assumable mortgages increases, lenders will likely continue to adapt their processes and innovate to meet the needs of borrowers. This could lead to the development of new loan products, streamlined application processes, and enhanced customer support, further improving the overall experience for buyers and sellers.

Regulatory Support and Guidance

The success of VA Circular 26-23-27 in reducing approval timelines for VA loan assumptions may inspire similar guidance and support from other government agencies, such as the FHA and USDA. Increased regulatory clarity and standardization could further boost the adoption of assumable mortgages and ensure a more consistent and efficient process across the industry.

Final Notes

Assumable mortgage approval timelines are dropping fast, thanks to recent changes and improvements in the industry. With streamlined processes, increased lender education, and clear regulatory guidance, buyers and sellers can now take advantage of the numerous benefits offered by assumable mortgages, including lower interest rates, reduced closing costs, and faster sales.

As the real estate market continues to evolve, assumable mortgages are likely to become an increasingly popular financing option, providing a much-needed alternative for homebuyers in a rising interest rate environment. By staying informed about the latest developments in assumable mortgages and partnering with AssumeList, buyers and sellers can navigate the assumption process with confidence and ease, ultimately achieving their homeownership goals while saving money along the way.

THE LCA BLOG

Weekly articles that cover every aspect of the real estate industry, growing your business, personal development & so much more.

Real estate teams are under constant pressure to generate leads, follow up with prospects, manage transactions, coordinate vendors, and provide a high level of service to clients. As a business grows, administrative work often increases faster than revenue-producing activities. This is why many successful real estate teams are combining artificial intelligence (AI) and virtual assistants […]

Key Takeaways Attention is the highest form of currency in 2026, and your social feed is where most of your future sellers are spending it. The agents winning listings right now are not the loudest posters or the ones running the fanciest ads. They are the agents who built a clear, niche real estate agent […]

Real estate agents have spent years building databases filled with homeowner contacts, but for many teams, those databases never become the business growth engine they were meant to be. Contacts pile up inside the CRM while agents focus on active clients, transactions, and new lead generation. Over time, valuable homeowner relationships go quiet, not because […]